A brief history of investing, an explanation of how we structure the boosst Portfolios & why we have not made any changes.

Last Updated: 26th March

We start with a history lesson…

When the very first companies offered shares for public purchase, the idea of growing wealth by investing was rather new. The East India Company is one of the earliest examples of a company that offered its shares for public sale, in 1602.

Through the late 19th and early 20th century, the predominant method of investing remained to purchase individual shares in companies. As more companies offered their shares publicly, investors could invest in a handful of companies and bring some diversification to their portfolio of shares.

It took until 1924 for the very first investment ‘Fund’ to become available. This meant that investors could simply purchase a single fund and leave the ‘Fund Manager’ think about which shares to purchase. This gave investors a selection of up to 50 companies in their portfolio and in return, the fund manager was paid a fee for their work. If a fund manager could obtain better information about a company than their competitors, or if their own analysis found that a company was undervalued, they could invest in that business on behalf of the investors to try and outperform other funds. Sometimes a fund manager was right, sometimes their analysis was wrong. This approach of buying a selection of companies within a market is called ‘active’ fund management.

In 1975, the first ‘Index’ fund was established by Jack Bogle. Bogle’s fund simply aimed to buy and hold a small part of the 500 largest companies listed in North America. By doing so, his fund was the first to achieve mass diversification. Index funds don’t pick individual shares or bonds to beat the market, they track the performance of the entire market. Or as he put it, “Don’t look for the needle in the haystack. Just buy the haystack!”.

With the advent of the internet, information became more readily-available to all. This meant that fund managers started to find it more and more difficult to get better quality information than others, so struggled to choose the right handful of companies to invest in, that could beat the performance of the whole market (the haystack!).

What approach do we take with your Portfolio?

By the very nature of an Index fund buying the whole market, it will consistently achieve ‘average’ performance every year. Some ‘active’ fund managers will beat the index in any given year and some may even consistently beat the market for a few years in a row. However our analysis concludes that where a very small proportion of ‘active’ fund managers do outperform the whole market consistently, it is impossible to tell if this is by skill or luck. The larger issue (regardless of skill or luck) is that there is no consistent method of identifying those fund managers and investing with them, before they beat the market. So at boosst, we don’t even attempt to pick ‘active’ fund managers, we use Index funds.

The boosst investment philosophy is built upon research from Nobel Prize winners Eugene Fama & Ken French, and seeks to consistently achieve an ‘average’ investment outcome. It is important to explain that ‘average’ is actually very exciting from an investment perspective.

Whilst it is okay to want a ‘better than average’ lunch or holiday, actively trying to achieve a ‘better than average’ investment outcome means that you must:

- Take substantially higher risks, as you have to choose a part of the market to not invest in … and if you get it wrong, you will lose some of your investment compared to the market.

- Pay significantly higher charges. ‘Active’ fund managers quite rightly ask for a fee for their work and they also incur transaction costs each time an underlying investment is bought or sold. Using ‘active’ fund managers is typically 4x the cost of a boosst portfolio.

Neither of these two attributes are desirable in an investment! We do not take this approach.

So in conclusion, a boosst Portfolio:

- Always achieves the ‘average’ performance of the global markets that we choose to invest in

- Saves significant fees compared to an ‘active’ alternative

- Benefits from mass-diversification and typically holds 11,000+ underlying investments

- Invests in local currencies around the world, to reduce reliance on any single currency

- Spreads investors funds around the world, investing in developed and emerging economies

- Includes commercial property exposure for added diversification

- Includes short-term loans to large companies and governments around the world. This provides a defensive element to a portfolio.

So what are we changing as a result of COVID-19?

Absolutely nothing.

There are two options available to investors who wish to change their investment approach in light of this pandemic:

Option 1: Pull out of the markets to protect from further losses and re-invest when this has all blown over.

Why we have not taken this action: This option is more commonly known as ‘selling to cash’. When uncertainty is peaking and markets are falling, the animal instincts of the human brain are awoken and it somehow feels ‘right’ to try and preserve what we have now and avoid further losses.

The problem with this approach is that you need to ‘time the market‘. Not only is doing so extremely difficult, but you also need to do it successfully twice.

For this decision to be beneficial you need to be certain that the market will continue to fall after you have sold to cash, otherwise you will have to re-purchase the funds at a higher price and you will have lost money. For the lucky few who do sell their investments at the right time (and markets continue to fall), they then need to choose when to come back in to the market and re-purchase. If investments fall further, do you leave it a little longer? If they rise, do you re-purchase and crystallise a loss? Or do you hope that markets fall again?

To make it even harder, there are transaction costs involved in both the sale and re-purchase of funds which will either reduce any gains you make or worsen any losses you crystallise.

If you want to try your hand at ‘timing the market’ to see how tough it truly is, try playing this simple game. CLICK HERE

Remember: It is important to sit tight, not sell to cash and remember that you still own everything you did before (the same number of shares in the same companies, and the same bonds holdings). Most crucially, a fall does not turn into a loss unless you sell your investments at the wrong time. If you don’t need the money, why would you sell? Falls in the markets and recoveries to previous highs are likely to sit well inside your long-term investment horizon i.e. when you need your money. Our Financial Planning based conversations will help ensure that we understand when you need to access your funds.

Option 2: Swap the underlying funds.

Why we have not taken this action: When equities (shares in companies) are falling in value and bonds (loans to governments and companies) remain stable or rise, it can be tempting to sell equity funds and buy bonds.

This is one of the worst decision that a long-term investor can make, as selling equities after they have fallen simply crystallises a loss.

boosst Portfolios already hold sufficient defensive assets (global bonds) to protect our more cautious investors from the worst of the market falls – so we do not need to rush and buy more bond funds now… we have been holding them the whole time!

boosst Portfolios are prepared for a market fall. Our more cautious portfolios hold more defensive assets, to create a smoother journey for investors who either do not want, or do not need, a volatile investment journey.

This all sounds obvious?

Good!

With the benefit of hindsight we can look back at any previous market fall, to see that this has always proven to be the best course of action.

But sometimes the hardest thing to do, is nothing. Which is why so many millions of investors get it wrong by allowing their emotions and human instinct to lead them in the wrong direction.

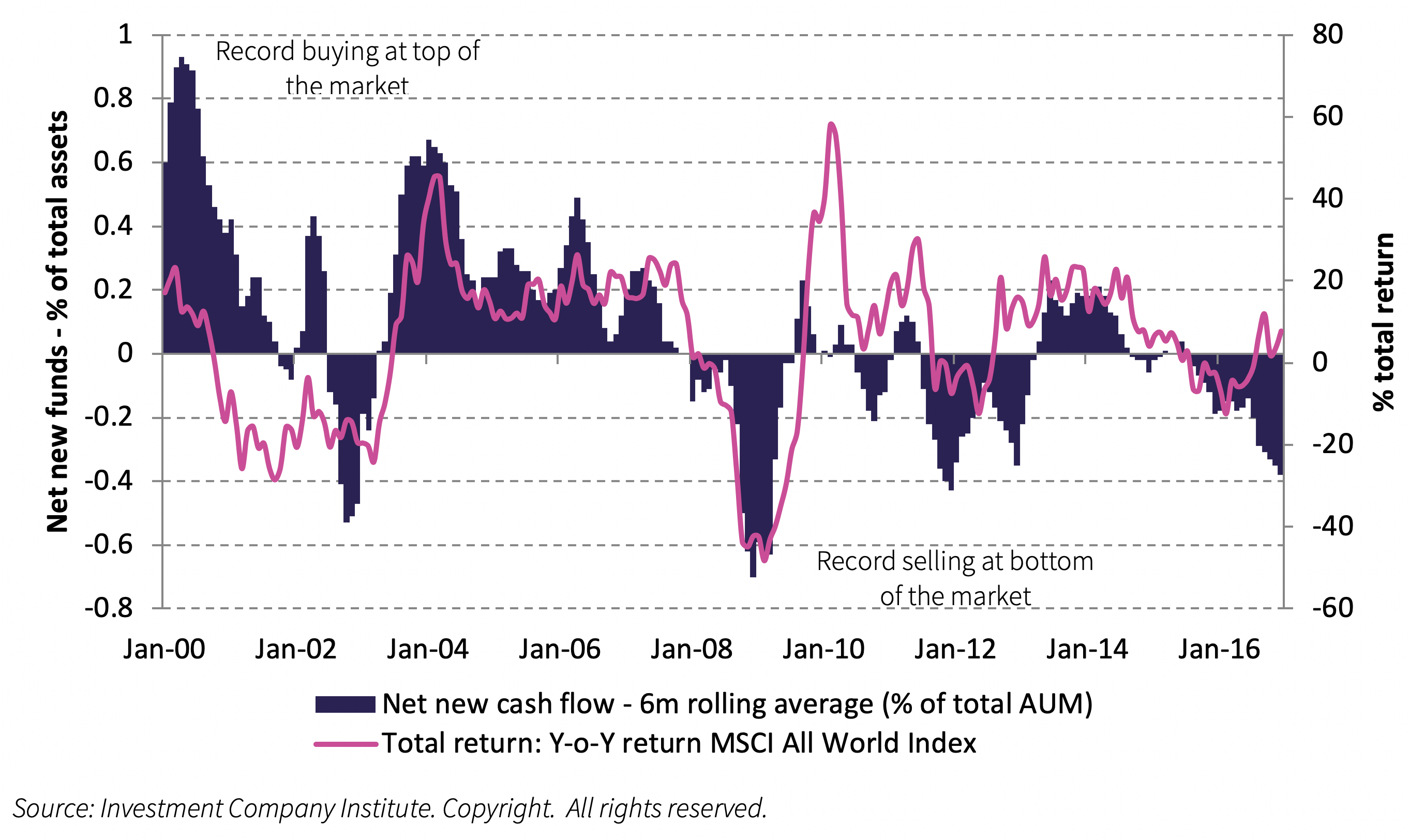

In the graph below, the pink line represents how the value of Global Companies fluctuated up and down. The purple bars show how investors reacted to these market movements. For example in 2004, when the pink line rises up, the purple bars also jump up, indicating that investors tend to buy more investments after they have seen them rise. Conversely in 2009, after investments had fallen by nearly 50%, the downward purple bars show that fearful investors around the world began pulling their money out of investments.

Staggeringly, investors love to buy investments after they have risen in value and sell them after they have fallen. A key part of our role is to help our clients avoid the very same trap.

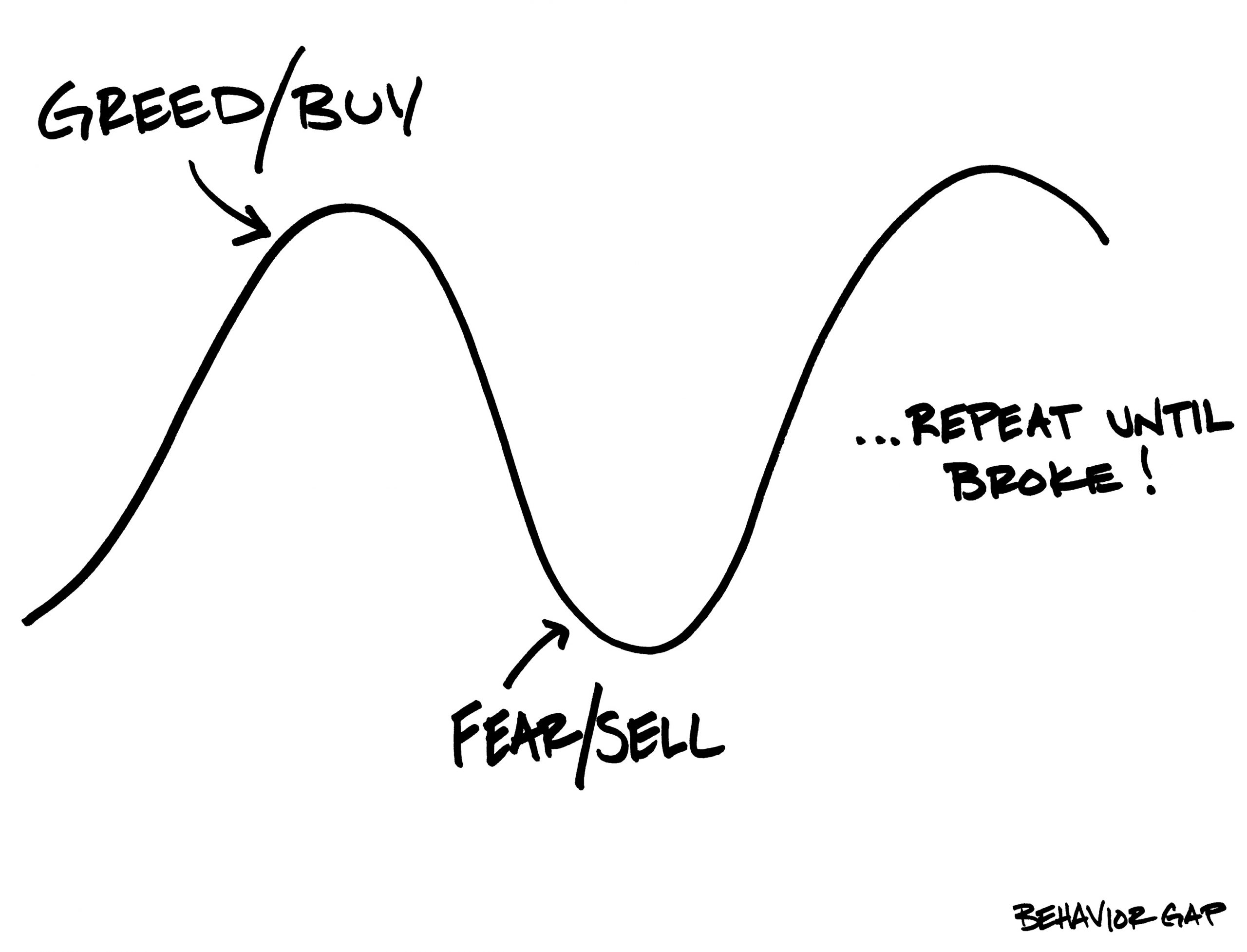

Here is a somewhat simpler sketch from Carl Richards which explains this concept perfectly:

Click here to return to our main ‘COVID-19 Thread’ and continue reading our latest thinking.

We thank you for the trust you have placed in us, and we hope you and your family remain healthy and safe.

Please be aware that the information we have shared in this Insight is for information purposes and is not individual advice. We make a conscious effort to check that all links to third party websites remain active and correct however we cannot take responsibility for their content or their availability.