We have updated this Insight to include changes to pension legislation that were introduced in March 2020, you can find the updated version of this Insight – HERE

Introduced in 2006 as a pension limit for the ‘top 1%’ of UK households, the Lifetime Allowance has become a real-life nightmare for some of the UK’s most loved professionals, including Doctors, Surgeons, senior Teachers and high-ranking Military Personnel.

It is clear that the Lifetime Allowance is no longer only impacting the UK’s ‘top 1%’.

This insight will help to explain how the Lifetime Allowance works, who is impacted and how we help our clients to plan for the Lifetime Allowance.

Research conducted in 2019 indicated that around 290,000 workers already have pension rights above the limit and well over a million more people are at risk of breaching it by the time they retire.¹

To understand the Lifetime Allowance, we should first remind ourselves of the Annual Allowance, as these two allowances operate together in tandem to control pension savings and limit the amount of tax-relief handed out by the UK government.

You can read our Pension Allowances – Part 1 insight, which focuses on the Annual Allowance – HERE.

So, how does it work?

There is no limit to the amount that can be saved in to pension schemes throughout your lifetime, as long as your contributions are within the Annual Allowance each year…

…however the Lifetime Allowance limits the amount of tax-relievable pension provisions an individual can accumulate. A tax charge applies to benefits in excess of the Lifetime Allowance to reclaim tax relief that you received when contributing, so it generally doesn’t make sense to build pension savings in excess of the Lifetime Allowance.

This means that you can in fact receive benefits greater than the lifetime allowance – and as your savings are not tested against the limit until retirement, it can be easier than you may think to sleepwalk in to having pension provisions in excess of the Lifetime Allowance.

The Lifetime Allowance is currently £1,055,000 and is due to increase by inflation each tax year. It is expected to rise to £1,080,000 in April 2020 however this is a lower limit than the Lifetime Allowance that was introduced in 2006 (£1,500,000) and much lower than the Lifetime Allowance in 2011 (£1,800,000). Each time that the Lifetime Allowance reduced in 2012, 2014 & 2016, Lifetime Allowance protection was available which enabled savers to retain a higher Lifetime Allowance. The vast majority of pension savers that did not work with a Financial Planner were unaware of the reductions or protection options available and now find themselves in a far worse position.

This table shows how the Lifetime Allowance has reduced over time:

Pension savers are only tested against the Lifetime Allowance when pension funds are withdrawn or accessed and the method of assessment against the Lifetime Allowance varies by the type of pension.

A pension which has a monetary value, such as a workplace pension, personal pension or a Self Invested Personal Pension (SIPP) is assessed each time funds are withdrawn before age 75.

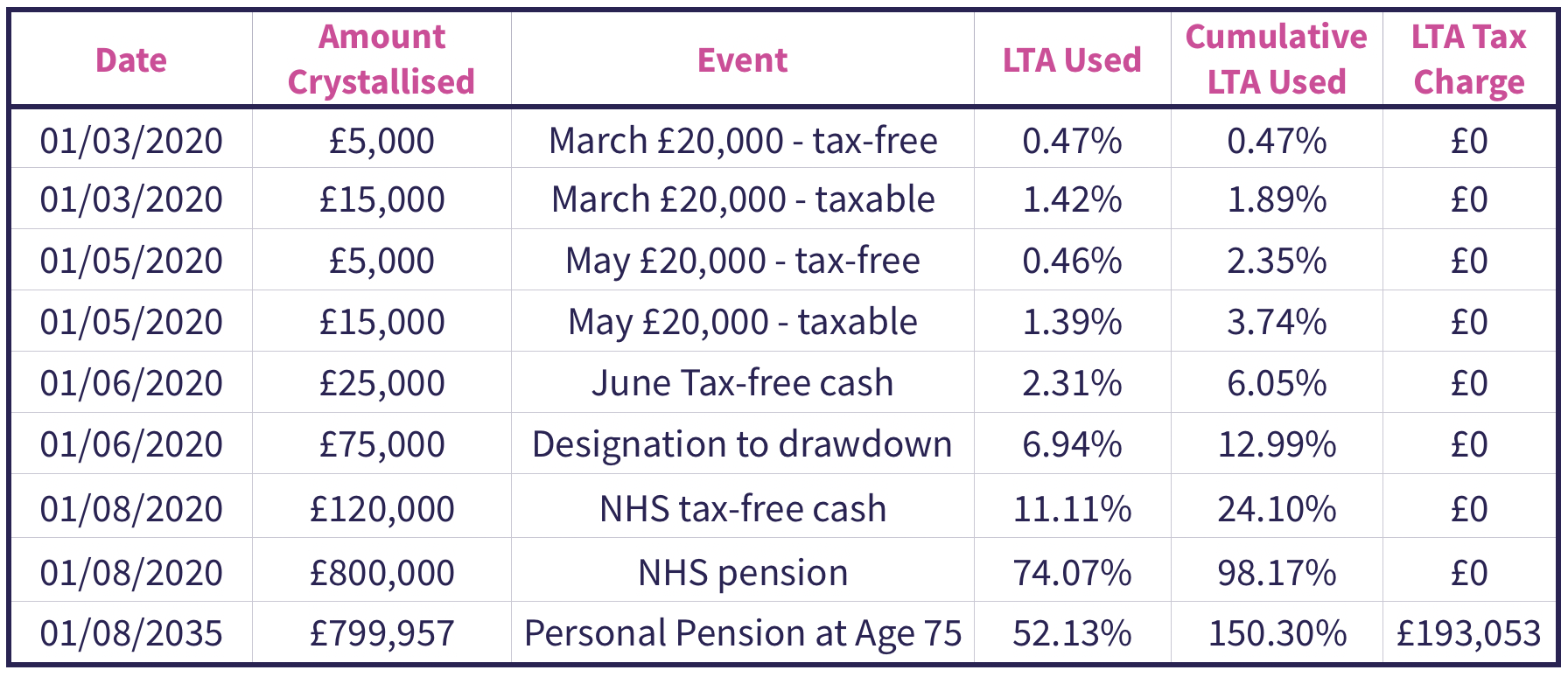

For example:

David is 59 years old, spent 25 years working within the NHS and has built personal pension savings of £450,000.

If he withdrew £20,000 in March 2020 as a standard pension withdrawal with 25% of the withdrawals as tax-free cash, this triggers a £20,000 test against the Lifetime Allowance.

£20,000 / £1,055,000 = 1.89% of the Lifetime Allowance used. David has 98.11% of the Lifetime Allowance remaining.

In May 2020, David decides to withdraw a further £20,000 in the same way…

£20,000 / £1,080,000 = 1.85% of the Lifetime Allowance used. As this withdrawal is after the Lifetime Allowance increase in April, David uses less of his lifetime limit for this withdrawal. David now has 96.26% of his Lifetime Allowance remaining.

A withdrawal which is tax-free cash only is treated differently.

If Dave withdraws a tax-free lump sum in June 2020 of £25,000, as it is all tax-free, he also crystallises a further £75,000 (the 75% of taxable income which would be attributed to this withdrawal).

So a £25,000 tax-free cash withdrawal crystallises £100,000 of David’s pension, using more of his Lifetime Allowance:

£100,000 / £1,080,000 = 9.26% of the Lifetime Allowance used. David now has just 87% of his Lifetime Allowance remaining. As he only withdrew the tax-free cash portion of the £100,000 that he has crystallised, when he later withdraws the £75,000 of taxable income, this is not tested against the Lifetime Allowance again.

David’s Final Salary pension is treated very differently:

As David also worked for the NHS for 25 years until 2015, with a salary of £96,000, he would be entitled to an NHS pension from his 60th birthday in August 2020 of:

25 / 60 x £96,000 = £40,000 per annum

(Formula is: “years service” / “scheme basis” x “final salary” = “annual income in retirement”)

Dave would also receive a tax-free lump sum equivalent to three times his pension income, so £120,000.

To test against the Lifetime Allowance, the annual pension amount that David receives is multiplied by 20 and the tax-free lump sum is added on top:

(£40,000 x 20) + £120,000 = £920,000.

£920,000 / £1,080,000 = 85.18% of the Lifetime Allowance used.

David only had 87% of his Lifetime Allowance remaining before the NHS Pension begun and after August 2020 he will have just 1.82% remaining.

Clearly David will exceed the Lifetime Allowance when he takes further funds from his Personal Pension, which will still have a value of around £310,000.

Even if David does not withdraw the rest of his personal pension, the value of all personal pensions are tested against the Lifetime Allowance one final time at age 75, which he will certainly have a charge applied.

What happens when you exceed the Lifetime Allowance?

All funds in excess of the Lifetime Allowance suffer a tax charge of either 25% or 55%.

If you opt to pay the lower rate of 25%, the funds are also subject to income tax when withdrawn from your pension. Alternatively, the 55% rate applies if you wish to withdraw pension funds as a lump sum with no further income tax.

A small positive is that the tax charge can be paid from the pension fund itself, so you do not need to pay the charge from cash savings or via self assessment.

Who is impacted?

Final Salary pension savers are most prominently impeded by the Lifetime Allowance as they have little control due to the calculation method.

The Lifetime Allowance has been featured in the media throughout the last 12 months as doctors, surgeons and GPs are being caught out by both the Annual Allowance whilst working and then the Lifetime Allowance at retirement.

At a time when the NHS is under more pressure than ever, it isn’t helpful that the Lifetime Allowance is pushing senior staff to retire, as they have already reached the lifetime limit for pension savings. Yet this is the reality facing thousands of senior NHS workers. With future pension savings facing (worst case scenario!) tax charges of up to 45% through the Annual Allowance and a further 65% via the Lifetime Allowance and income tax, there really is very little motivation to continue working.

This very same issue also impacts senior teaching staff, British Airways pilots and senior military personnel.

Crucially, it also impacts government officials, so we may finally get some movement in the upcoming Chancellors Budget in March.

Unlike Final Salary pension savers, whose pension entitlement is dictated by years of service and their scheme salary, Individuals saving for retirement with ‘standard’ pensions which hold a monetary value (workplace pensions, personal pensions & SIPPs) have more control when it comes to the Lifetime Allowance. However this doesn’t mean that they are immune from the Lifetime Allowance.

Pension savers can find themselves breaching the Lifetime Allowance, here are some examples of those at risk:

- Individuals who made large contributions in the 80’s and 90’s, before a Lifetime Allowance was introduced

- Those who planned on a Lifetime Allowance of at least £1,800,000, as we had in 2011 – but did not apply for protection when it was available.

- Individuals who have large pension funds, successfully applied for Fixed Protection in 2012, 2014 or 2016 but lost their protection by being automatically-enrolled into a new workplace pension scheme. (New contributions invalidate any existing Fixed Protection!)

- Those who have invested their pensions well! A decade of strong equity growth since the last global recession has pushed some savers far beyond the standard Lifetime Allowance

How can boosst help?

Projecting Lifetime Allowance is a valuable part of our service for clients, which can help us to identify pension over-funding decades in advance of a tax charge arising.

We use planning tools specifically designed to plan for and mitigate future Lifetime Allowance tax charges and structured planning has enabled us to help savers to avoid suffering unnecessary tax charges.

Here is an example for David:

Planning for the Lifetime Allowance can be tricky, as there is always the risk that the current rules and limits will be changed, as they have been in the past. Our ongoing service and annual planning meetings are fundamental for us to keep clients finances ahead of upcoming changes and ensure that allowances are being optimised.

If you are not a client but feel that you should seek advice after reading this, please contact us. We can setup a call for you with one of our Financial Planners to explore your current position and explain how our services can help you.

Published in February 2020.

The content of this blog post is based on our current understanding of UK legislation and applies to the 2019/20 tax year. This article should in no way be considered as personal advice.

If you have any questions whatsoever, please contact us: hello@boosst.financial

¹ https://www.royallondon.com/media/press-releases/2019/march/groundbreaking-new-research-reveals-lifetime-allowance-timebomb-set-to-hit-more-than-a-million-workers/