Long-term goals… short-term emotions!

Goals & Emotions

As a client of boosst, there is always a tension that exists between the sensible, well-thought-out long-term financial goals that you set for yourself – often at our annual planning meetings – and the emotions that you are likely to experience in the moment, as markets respond to new information and portfolio values are impacted.

This tension is most obvious in the early stages of our relationship – especially when a portfolio either goes down, or sideways in the first year or so. As much we all want your first investing experience to be a positive one (with markets rising), in reality this is obviously not always the case, as newer clients have recently experienced.

From your point of view, an aversion to loss, the feeling of loss of control and disappointment at seeing hard earned money falling in value can feel unsettling. From our perspective it can also be a challenging time, knowing that however sound the financial plan we have built for you, however sensible the portfolio asset allocation and however much time we have spent providing insight into the up and down journey you will experience, emotions often trump logic when a portfolio shows a fall in value.

Whenever markets are having a dip – use these four steps to remind yourself of why ‘no action’ is the best action:

- First, cash is the only investment that avoids losses, but only before inflation, and its low, long-term, after-inflation returns are unlikely to allow most investors to meet their financial goals, hence the need to add equities and bonds into the asset allocation. Do not be fooled by today’s high cash rates relative to recent years; cash returns are the ultimate enemy in disguise for long-term investors and are not a substitute for a sensibly structured long-term portfolio designed to meet long-term goals. Do not be tempted by them.

- Second, it is the very uncertainty of the shorter-term outcomes of equities and bonds that delivers the longer-term, higher after-inflation returns that most of our clients need to meet their goals. The longer-term expected returns from a sensibly structured investment portfolio are far higher than those of cash.

- Third, returns come from markets not financial planners. Blame should not be apportioned to a financial planner because a portfolio has gone down, in the same way that we do not seek praise if it has risen spectacularly! Markets are not predictable in the short term. Stay invested.

- Finally, falls in portfolio values are not losses and have every likelihood of recovering in time. Patience allows the longer-term expected returns to be realised. Avoid emotionally driven investment decisions that might impact these longer returns.

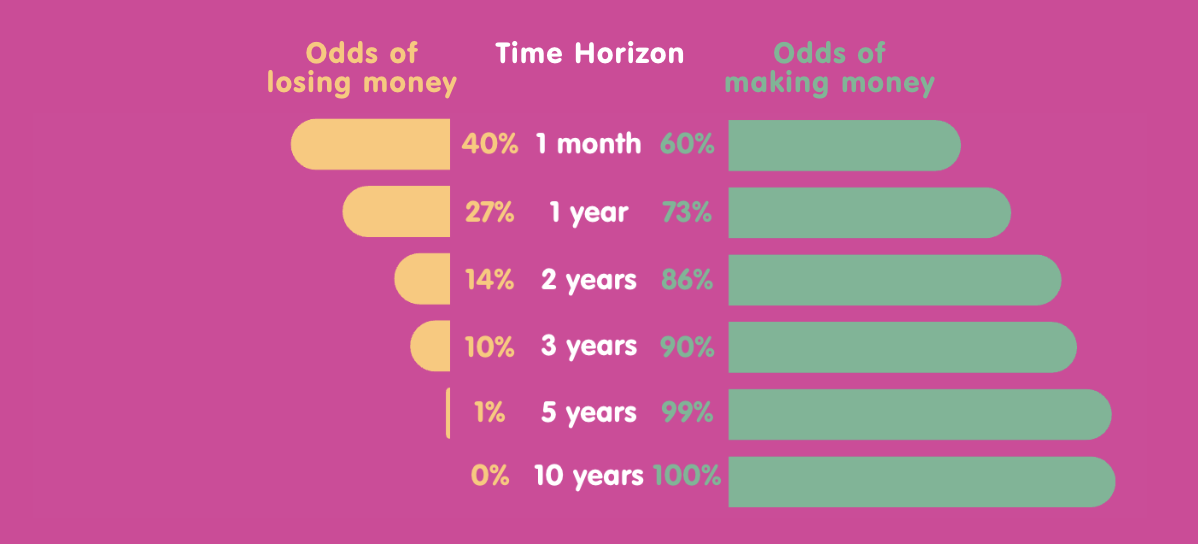

So what are the odd’s?

The chart below shows the proportion of times that investors in our boosst 60 portfolio (that’s a balanced portfolio, with 60% equity & 40% short-term bonds) have suffered falls in value over different time horizons.

Whilst falls in purchasing power (i.e. after inflation) over two years are not uncommon, over five years – which is only a fraction of the time horizon of most investors – the chances of a fall decreases materially. This diagram is based the last 30+ years of data available and is after accounting for fees and inflation.

Interestingly, whilst some might think that the data above looks ‘too good to be true’, it’s important to recognise that investors only achieved these outcomes if they stayed invested. To give yourself the best chance of improving your ‘odds of making money’, you too must stay invested.

It is also worth highlighting that those who were invested over these 30+ years would need to have accepted 12 month returns varying from +56% to -31%. Overall, their average annual return would have been 5.5%, above inflation, after fees. Please keep in mind that this is all past data, and is no projection or statement about the future.

What should you do?

If you are a new investor, keep the faith and remain invested for the long term – because that is what is required to give yourself a chance of meeting your long-term goals. If you have been investing for some time and been through one of more cycles of market falls and recoveries, hopefully the tension between longer-term goals and short-term emotions will be greatly tempered.

As Charlie Munger, Vice Chairman of Berkshire Hathaway once said:

‘The big money is…in the waiting’

Footnote:

It’s no secret that more anxious investors will login to check on their portfolios more often… which of course is a vicious circle. We see this habit all of the time. Our more relaxed clients, typically those who have been a client for 3+ years, will have seen the up’s and down’s of their portfolio and come to realise that those movements are perfectly normal and to be expected… so never login!

Risk warnings

This article is distributed for educational purposes and should not be considered investment advice. This article does not represent a recommendation of any particular fund, strategy, or investment product. Information contained has been obtained from external sources and is believed to be reliable but this is not guaranteed.

Past performance is not indicative of future results and no representation is made that the stated results will be replicated.