‘You Asked’ is a series of insights from the boosst team. You, our clients, have a wonderful ability to ask relevant and thought-provoking questions… which are often (but not always!) related to financial planning. boosst is a trusted source of knowledge and independent advice, so it makes sense that you come to us with a broad range of questions – which can vary from ‘Which car should I buy?” to “What’s the best way to teach our children about money?”.

This ‘You Asked’ post was written by Josh.

You Asked: Why do we use shorter-dated, high-quality, hedged bonds?

Bonds play an important role in most investors’ portfolios, providing more cautious investors with more certain outcomes than equities, at the price of lower returns. Their main role is to offer some downside protection at times of equity market trauma. But not all bonds are equal – and they range from cash-like to more equity-like. So, the type held in your portfolio is very important. Let’s take a look at the three key choices in turn.

Choice 1: Shorter vs. longer

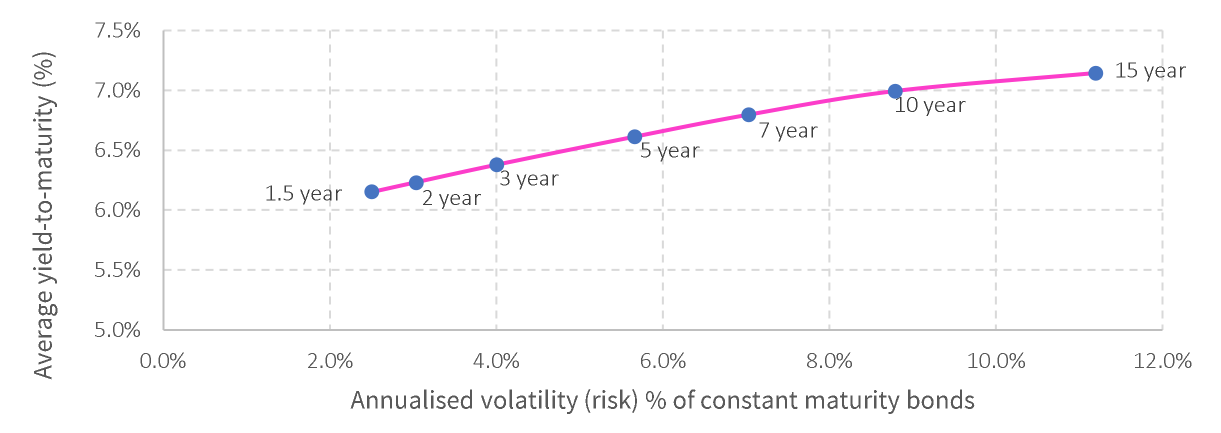

Over time, the return that you receive from owning bonds is closely related to the ‘yield-to-maturity’ at the time you buy them. If you hold a bond to its maturity date, that is the return you will receive assuming all coupon (interest) payments are reinvested. Using UK government bond (gilt) data from 1970, we can run a simple analysis and look at the average yield-to-maturity of bonds from 1.5 years maturity up to 15 years. The results are plotted below, against the volatility of returns of a constant maturity bond portfolio at each chosen maturity. It is clear to see that there is only a small benefit in terms of ‘increased yield-to-maturity’ (around 1%) – but the risk level (annualised volatility) picks up dramatically. It is worth highlighting that the annualised volatility of returns (risk %) of global equities was measured at around 15%. On this basis, 15-year bonds had around three-quarters of the risk of global equities compared to just over one-third for 5-year bonds.

Figure 1: Shorter-dated bonds have favourable risk-to-reward characteristics (1/1970-3/2023)

Choice 2: High quality borrowers vs. low quality borrowers

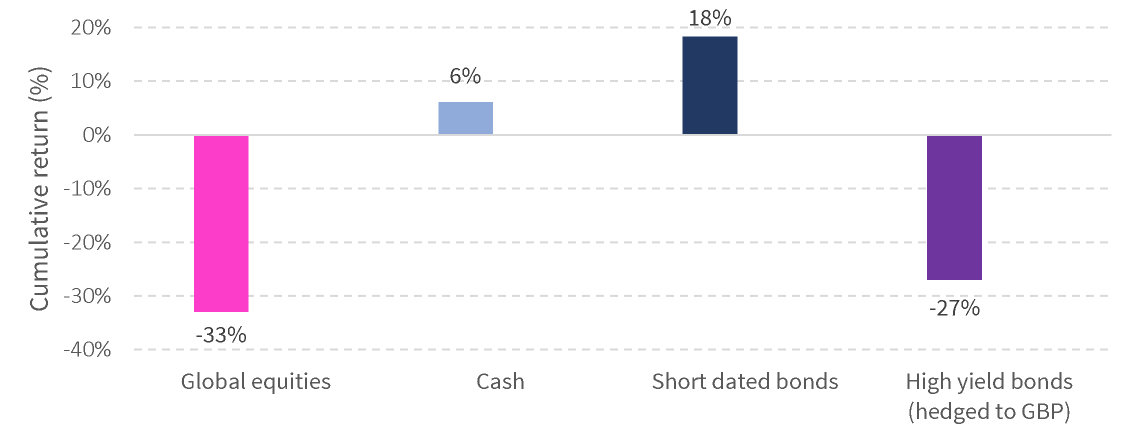

Regardless of whether a portfolio is more cautious or more adventurous, the role of the bonds held remain the same – they are the defensive part. Sure, a more aggressive portfolio will hold far less bonds, or maybe even none, but the role of the bonds held is still the same – to be defensive and reduce overall portfolio volatility. As you move away from the strongest borrowers (AAA and AA), yields rise as borrowers become weaker. If you slip below investment grade (any bonds rated below BBB) into ‘high yield’ bonds, you are taking on a greater degree of the risk. Lower quality corporate bonds have an increasing correlation to the borrower’s equity, reflecting the risk of default on their debt. At times of equity market crisis – when weaker companies may be in trouble – higher quality bonds tend to perform better than lower quality bonds, providing a useful defensive holding in a portfolio, as the figure below illustrates.

Figure 2: High quality bonds offer defensive qualities – Global Financial Crisis 11/07 to 2/09

Choice 3: Hedged vs. unhedged

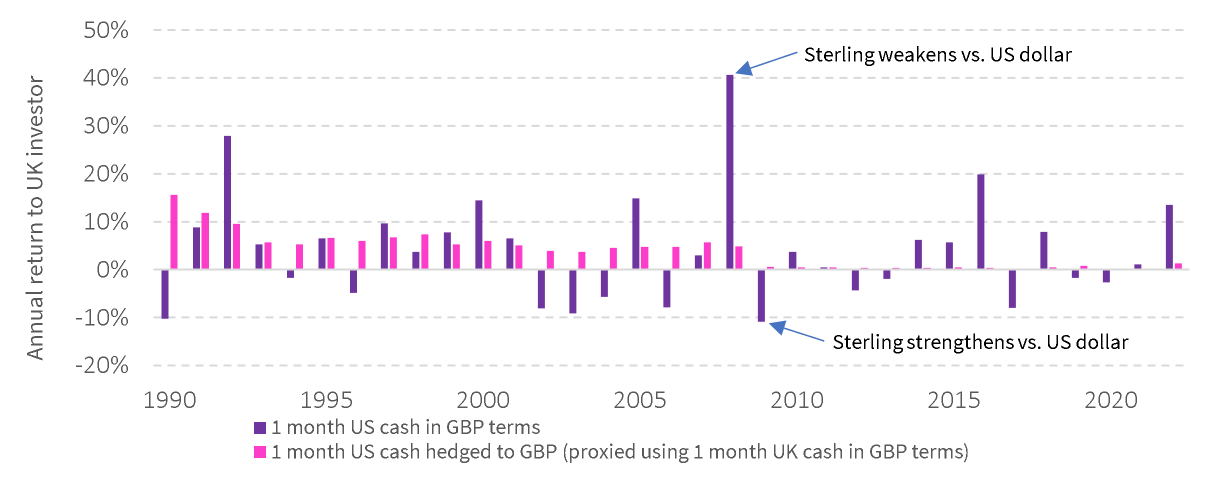

Buying foreign bonds increases the available range of bonds for investors and diversifies the risk of interest rate movements across markets. A foreign bond comes with currency risk between the currency of issue (e.g. US dollars) and the base currency of the investor (e.g. Sterling for a UK investor). Currency exposure introduces an equity-like risk into the bond portion of portfolio, creating a volatile asset, which is not what we want for the defensive part of a portfolio!

Let’s run a quick experiment. For simplicity’s sake, imagine that you placed a deposit in US dollars for one month and rolled it over each month without hedging the currency, from 1990 to 2022. Imagine too, an alternative scenario where you hedged the US dollars back to GBP, in effect ending up with a synthetic GBP cash deposit, as the cost of hedging is calculated using the difference between the two interest rates (unfortunately there are few free lunches in investing!). The chart below reveals the material difference in annual outcomes. As the pink bars are much smaller, we can see that by hedging we can greatly reduce the impact of currency exchange rates on the investors bond returns, which is precisely what we seek.

Figure 3: Currency adds material volatility to the equation (1990-2022)

In conclusion:

- We feel that all investors need to be able to talk themselves out of a sensible starting point; shorter-dated, higher-quality, currency-hedged bonds. We’ve explored all of the options and can’t talk ourselves out of this very sensible approach to the defensive portion of a portfolio.

- We don’t expect zero volatility from bonds and we also don’t expect the returns from bonds alone to outpace inflation. We do however expect bonds to provide a smoothing effect which allows investors with a lower appetite for risk (price volatility) to invest some of their portfolio in equities, and give themselves a solid chance of matching or outpacing inflation.

- At the time of writing in May 2023, bonds have had a poor 18 months – with banks around the world increasing interest-rates, which makes the existing bonds in circulation less attractive to investors. Thankfully our portfolios use shorter-dated bonds, which have been impacted the least by this trend.

- Over time, now that interest rates (and therefore yields) have risen for the first time in over a decade, going forward we will see companies and governments needing to pay lenders (investors!) more interest, which will mean that bonds have a greater contribution to returns in the future, compared to what we have become used to.

We hope this guide has been helpful! As always, if you have any questions, our team will be very happy to assist.

Risk warnings

This article is distributed for educational purposes and should not be considered investment advice. This article does not represent a recommendation of any particular fund, strategy, or investment product. Information contained has been obtained from external sources and is believed to be reliable but this is not guaranteed. Past performance is not indicative of future results and no representation is made that the stated results will be replicated.